Controlling as a Function of Management

After you watch the video and know the material, click HERE for the quiz.

In this lesson, we will explore the role of controlling as a function of management and its use of various control mechanisms to reach organizational goals.

Background: The Management Process

Controlling is the fourth step in the management process. Let's review the process as a whole to better understand how controlling fits.

The first step, planning, involves developing short- and long-term goals for the organization. This includes setting goals and planning for the necessary resources needed to attain the set goals. Goals can be short-term, like a sales blitz, or long-term, like developing a new marketing plan. Either way, managers begin by first planning for the goals.

The next step, organizing, involves performing all of the tasks needed to get the job done. This means gathering all of the resources, like people, capital and information, so that everything is ready when needed.

The next step, directing, involves actually executing the plan - putting all of the resources to work to achieve the short- and long-term goals set forth in the planning stage.

The final step, and the main focus of our lesson, is controlling. It involves comparing actual performance to expected performance.

|

Controlling as a Process

The controlling process involves:

- Establishing standards to measure performance

- Measuring actual performance

- Comparing performance with the standard

- Taking corrective action

Controlling Process Explained

The controlling process is simply a set of steps a manager uses to determine whether organizational goals have been met. Let's explore each step of the process and apply examples to demonstrate its function for management. Let's use the example of TQM Auto Repair Shop to understand the controlling process.

Establishing Standards to Measure Performance

This involves making decisions about the goals an organization wants to focus on during a period of time. These can be financial, customer satisfaction, production or employee performance-related goals.

Measuring Actual Performance

This involves creating measuring tools to collect data. The tool should be able to report on performance as it relates to the standards set, or 'measures,' developed in the first step of the controlling process. These tools can be a balance sheet, a sales report, data collected from a customer satisfaction survey or even an employee performance appraisal.

|

Comparing Performance with the Standard

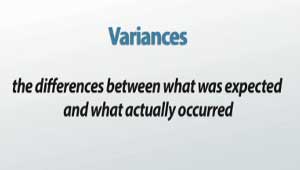

This involves comparing 'actual' performance to performance standards based on data collected in the second step of the controlling process. Using the measuring tools created in the second step, managers are able to compare current performance and productivity to the standards set. A manager may want to compare sales performance from last year to this year by comparing the actual sales from the previous year to the sales of the current year. This comparison tells a manager whether the sales team is below, meeting or exceeding goals. These are called variances, or differences between what was expected and what actually occurred.

|

Taking Corrective Action

This involves determining whether changes need to be made, what changes need to be made and devising a plan for making changes. Managers will use comparisons to determine what needs to be investigated. If sales are lower than expected, managers will look at various things.

Perhaps the salespeople are not making as many client calls as they did last year. In this case, corrective action may be taken against the employees for non-performance. A manager may look at the work itself. Maybe there are too many clients and not enough staff. In this case, a manager may have to hire more staff. The price of the product or service may be too high, and it may affect demand. In this case, a manager may have to look at ways to add value to a product or service or lower prices.

Controlling Process in Action

Let's look at examples of the controlling process in action. Sam, the manager of TQM Auto Repair Shop recently set goals for his business. First, Sam must establish standards, or a set of 'requirements' for his business. Sam is working on the first step, establishing standards to measure performance.

Sam wants to make $100,000 more this year that he did last year so he can replace older equipment in the repair shop. Raising the price of repairs can do this. This is a financial goal.

It is important not to take customers for granted. A goal to increase customer satisfaction from 84% last year to 90% this year is set. Customer service satisfaction must increase by six percent this year. This is a customer service-related goal.

Sam sets a goal to increase the quota, or a goal set for production, for the amount of cars each mechanic must repair each week. This is a production goal.

With all of the new goals Sam set for the repair shop over the past week, employees may not be able to keep up with the workload. To ensure the goals are met, Sam must devise a way to measure the productivity and performance of his employees. This measurement is compared with the goals he set above, or the preset standards. Once he evaluates the information, Sam can provide feedback to each employee. This will help them make improvements to their work. This is an employee performance appraisal.

Sam developed the standards for what he would like to accomplish in the above step. Now, he needs to develop a way of determining whether the goals are being met. Sam creates a new pricing guide, a customer satisfaction survey, a sales quota system and an employee evaluation system. Sam is working on the second step, measuring actual performance.

Sam will present the new pricing guide to employees. He explains his plan for raising much-needed revenue to each employee so the employee understands the reason for the price increase. It is important to include employees in setting goals. If Sam's employees understand the reason for the price increase, they will be more likely to buy-in to the goal.

Sam also introduces the customer satisfaction survey to his customers. Each customer will fill out a survey where they will rate their experience based on many factors like:

- Timeliness of repairs

- Quality of work

- Price

- Friendliness of mechanics

- Ease of payment

Sam also has to develop a way to measure how many cars are being repaired by each mechanic on a weekly basis to be sure that the amount of repairs done weekly, monthly and in a year add up to the desired goal of increasing revenue by $100,000 set forth above. He introduces the mechanics to a repair quota system. Each mechanic must fix ten engines, patch five tires and replace 15 windshield wipers each week. That means that each mechanic must bring in about $280.00 in revenue each week to reach the goal. Once broken down for the mechanics, the goal is realistic and attainable.

The toughest challenge for Sam will be to introduce the employee appraisal system. He uses a system that involves the employee setting goals for themselves and Sam setting goals for the employees. After chatting with each employee, Sam is able to determine the criteria for acceptable performance. He will include the sales quota system from above, dependability, reliability, motivation and absenteeism in the appraisal. He will sit down with each employee to explain the process. If employees have input in setting goals for themselves, they are much more likely to achieve the goals.

|

As time goes by, Sam needs to monitor the process to be sure it is working. Sam is comparing performance with the standard. Sam reviews his repair receipts and income statements each month to be sure he in on target for his financial goal of increasing revenue by $100,000.

Sam also reviews the customer satisfaction surveys each week. He documents the percentages in a spreadsheet. He compares each survey percentage change with that of the previous year to determine whether there are positive changes in customer satisfaction.

Sam reviews the daily and weekly receipts to determine whether the mechanics are meeting their quota set above. He documents the various work done by each mechanic on a spreadsheet. He compares this to the standard he set in the first step.

Finally, Sam needs to be sure that employees are meeting their goals set in the employee appraisal. While this cannot be done frequently, like counting receipts or crunching numbers, it can be done every six months to a year. When the time comes, Sam will sit down with each employee on an individual basis to discuss progress towards the goals they set together. He will compare the actual progress toward the standard set for each employee.

There is no doubt that some of the actual performances will fall short of the standards set in the first step. When this occurs, Sam will have to make important decisions. He will make changes in the way things are being done. In other words, he will be taking corrective action.

For instance, if Sam determines that the price increases are causing customer satisfaction percentages to plummet, he will need to restructure pricing or change the level of service. Maybe it is as simple as providing customers with a free lunch while they wait. It could be that Sam will have to decrease prices to retain his customers. He may even have to look for new customers.

Sam may determine that employees just can't keep up with their quotas. Sam will have to revisit the quotas. Perhaps the shop needs to be reconfigured so employees can maneuver around the cars more efficiently. Perhaps Sam needs to discipline mechanics that are not keeping up the pace.

Whatever decisions Sam makes, he will have to go back to the drawing board and begin the controlling process all over again.

Lesson Summary

|

In summary, controlling as a management process involves setting appropriate goals for various areas of the organization. These goals can be financial, customer satisfaction-related, sales-related and employee performance-related.

Once goals are set, managers begin developing measuring tools to gather data for each goal. There are many tools that can be used. Some tools are a balance sheet, daily receipts, customer satisfaction surveys, sales quotas and employee appraisals.

Once the tools have been developed and the data is gathered, managers begin comparing the goals to the actual results. Almost in a side-by-side fashion, goals and actuals will be evaluated. Managers will look for variances in numbers, amounts, percentages, performances and productivity.

Finally, managers will chart any negative variances to determine what needs to change by taking corrective action. This may be a pricing change, an added value to a customer, a new target market or even disciplining employees.

The controlling function of the management process does not end here. The management process as a whole is continually revisited at different intervals. It is an evolving process that is repeated until all of the organizational goals have been met.